I created a “debt denial” checklist to figure out how deep I was in trouble. Here are the 10 warning signs I ignored and how you can face the truth today.

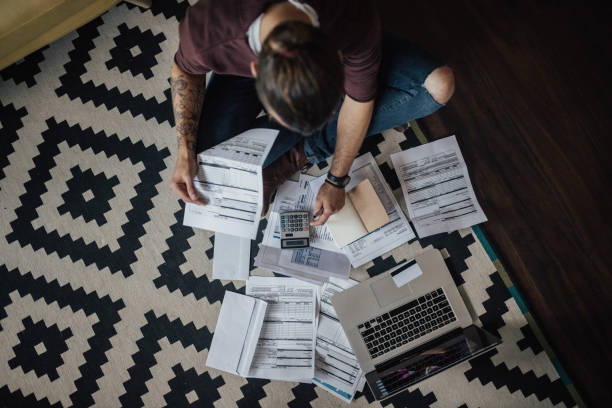

I remember the exact moment I knew I needed a serious “debt denial” checklist. I was sitting on my living room floor, surrounded by unopened envelopes. I had been stacking them there for weeks, telling myself I would get to them “this weekend.” But the stack kept growing, and my anxiety kept growing with it. I knew what was inside those envelopes. They were bills. They were credit card statements. They were collection notices. And I was too scared to look. I was living in a fog, pretending everything was fine, even though my stomach was in knots 24 hours a day.

That fog has a name. It is called debt denial. It is that feeling of knowing something is wrong but convincing yourself it is not that bad. It is the art of looking away. And it almost ruined me. If you are reading this, you might be in that same fog. You might be wondering, “How deep am I?” I wrote this “debt denial” checklist to help you find out. I am going to walk you through the ten signs I ignored for years. Be honest with yourself as you read them.

Sign #1: The Unopened Mail Mountain

The first sign on my “debt denial” checklist was the mountain of unopened mail. I stopped opening envelopes because I knew they contained bad news. I would sort through the mail, separate the junk from the bills, and then put the bills in a pile on my desk. That pile grew and grew. I told myself I was “waiting for the right time” to deal with it. But the right time never came.

I remember one specific letter that had a red “FINAL NOTICE” stamp on it. I saw it, felt a wave of panic, and literally buried it under a magazine so I wouldn’t have to look at it. That is denial in action. If you have unopened bills sitting in a drawer, on your desk, or in a pile anywhere in your home, check this sign off on your “debt denial” checklist.

Sign #2: The Minimum Payment Trap: The “Debt Denial” Checklist

The second sign was the minimum payment trap. For years, I made only the minimum payment on my credit cards. I told myself I was being responsible because I was paying something. I was keeping the accounts “in good standing.” But I was fooling myself.

I never looked at how much interest I was paying. I never calculated how long it would take to pay off the balance at that rate. I just saw the minimum number and paid it, thinking I was safe. In reality, I was treading water in a deep ocean. The debt wasn’t shrinking. It was growing, thanks to compound interest. If you only pay the minimum and hope for the best, you are deep in denial. This is a critical item on the “debt denial” checklist.

Sign #3: The “I’ll Fix It Tomorrow” Lie: The “Debt Denial” Checklist

I was a master of procrastination. I constantly told myself, “I’ll fix it tomorrow.” I would have moments of clarity—usually at 3 AM when I couldn’t sleep—where I would swear to myself that I would call a credit counselor, or create a budget, or sell some stuff. But when morning came, I would talk myself out of it.

I would think, “It’s not that bad.” Or, “I’ll wait until after the holidays.” Or, “I’ll start fresh next month.” Tomorrow never came. Procrastination is the engine of debt denial. It keeps you stuck in place while the problem gets worse. If “I’ll fix it tomorrow” is a phrase you use regularly, add it to your “debt denial” checklist .

Sign #4: Hiding Purchases from Loved Ones: The “Debt Denial” Checklist

This one hurts to admit. I started hiding purchases from my partner. It wasn’t big things. It was takeout food when I said I would cook. It was a new video game I didn’t need. It was clothes that I would sneak into the house and hide in the back of the closet.

I told myself I was just avoiding an argument. But really, I was avoiding accountability. I knew I shouldn’t be spending the money, so I hid the evidence. Secrecy around money is a huge red flag. If you find yourself hiding receipts, deleting emails, or lying about what things cost, you are in denial. This is a painful but necessary part of the “debt denial” checklist .

Sign #5: Avoiding Bank Account Logins: The “Debt Denial” Checklist

I used to go days, sometimes weeks, without logging into my bank account. I would get paid, spend money, and just hope that the math worked out. I was terrified of seeing a low balance or an overdraft fee.

I remember one time I went almost two weeks without checking. When I finally logged in, I had three overdraft fees and a negative balance. I had been swiping my card, thinking I had money, when I was actually in the red the whole time. Avoiding your account is not a strategy. It is a symptom. If you dread logging in, you need this “debt denial” checklist .

Sign #6: Making Excuses Constantly

My brain was a factory of excuses. “Everyone has debt.” “It’s just how things are these days.” “I deserve to treat myself.” “The economy is bad, it’s not my fault.” Some of these excuses even had a grain of truth. Yes, many people have debt. Yes, the economy can be tough.

But excuses don’t pay off balances. They just keep you comfortable in your misery. I used excuses to justify inaction. I convinced myself that my situation was normal, so I didn’t need to change. If you find yourself defending your debt instead of fighting it, you have another checkmark on your “debt denial” checklist .

Sign #7: Using One Card to Pay Another

This was the moment I knew I was in trouble, even though I refused to admit it. I started playing the “credit card shuffle.” I would take a cash advance from one card to make the minimum payment on another. I would apply for a new card with a 0% balance transfer offer, move the debt, and then run up the old card again.

I felt like I was being smart, like I was gaming the system. In reality, I was digging a deeper hole. I was paying transfer fees, juggling due dates, and living in constant chaos. If you are using debt to pay debt, you are not managing your finances. You are surviving a crisis. This is a major red flag on the “debt denial” checklist .

Sign #8: Feeling Sick When Thinking About Money

My body knew I was in denial before my brain did. I would get a knot in my stomach every time money came up in conversation. If my partner said, “We need to talk about the budget,” I would immediately feel nauseous and defensive. I would snap at them or change the subject.

I had trouble sleeping. I would wake up at 3 AM with my heart racing, thinking about bills. I was irritable and stressed all the time. I didn’t connect this to debt at first. I thought I was just “anxious.” But it was the debt. It was the weight of the secret I was carrying. If money makes you physically ill, you are in denial .

Sign #9: Living Paycheck to Paycheck (and Calling it Normal)

I normalized living on the edge. I would get paid on Friday, and by Monday, most of the money was already spoken for by bills and past-due payments. I had no savings. None. If I had a flat tire or a medical bill, I would have to put it on a credit card, adding to the pile.

I told myself this was just “adult life.” I thought everyone lived like this. But it’s not normal. It’s a sign that your expenses exceed your income, and you are using debt to fill the gap. If you are one emergency away from disaster, you need this “debt denial” checklist .

Sign #10: Not Knowing the Total Number

Here is the biggest one. For years, I could not have told you my total debt. I knew I had a few credit cards and a car loan. But if you had asked me for the exact total, I would have guessed low. I avoided adding it up because I was afraid of the number.

I was afraid that if I saw the real total, I would panic. But here is the truth: the number is already real. Not knowing it doesn’t make it smaller. It just makes you powerless. The day I finally added up every single debt—every credit card, every loan, every missed payment—was the day my denial started to crack. The number was terrifying. But it was also the truth. And the truth, as painful as it was, set me free. If you don’t know your total debt number, you are in denial. This is the final and most important item on the “debt denial” checklist .

How I Finally Faced the Music

After I checked off every single item on my own “debt denial” checklist, I had a choice. I could go back to sleep, or I could wake up. I chose to wake up. It wasn’t easy. It was one of the hardest things I have ever done. But it was also the most necessary.

I started by gathering every single statement I could find. I opened every unopened envelope. I made a spreadsheet. I listed the creditor, the balance, the interest rate, and the minimum payment. I totaled it up. I stared at the number. I let myself feel the fear and the shame. And then I made a plan.

I called a non-profit credit counseling agency . I talked to someone who didn’t judge me. We worked out a debt management plan. I cut up my credit cards. I stopped using the “shuffle.” I started paying more than the minimum. It took years. Years of sacrifice, of saying no, of driving an old car and eating at home. But slowly, the number started to go down.

What You Can Do Today

You don’t have to wait until you hit rock bottom. You can use this “debt denial” checklist right now to assess where you are. Be honest. How many of these signs are true for you? If it’s more than a few, it’s time to act.

Start by opening one envelope. Just one. Log into one account and look at the balance. Write it down. That is the first step. You don’t have to solve everything today. You just have to start looking. The fog starts to clear the moment you stop looking away.

The Freedom on the Other Side

I am on the other side of that fog now. I have savings. I have peace of mind. I sleep through the night. I can talk about money without my stomach hurting. I am not special. I am not a financial genius. I was just a guy who was deep in denial and finally decided to stop running.

You can do this too. It starts with admitting how deep you are. Use my “debt denial” checklist. Be brave. The truth won’t kill you. It will save you.

For more tools, resources, and community support to help you face your debt and build a better future, visit evdrivetoday.com. We share real stories and practical steps to help you take control.

Let’s Talk About Your Checklist

Now I want to hear from you. How many items on this “debt denial” checklist hit home for you? Which one was the most painful to read? Have you ever added up your total debt? Are you scared to do it?

Drop a comment below and share where you are on your journey. This is a safe space. No judgment. Just people helping people wake up and take control. Your comment might be the thing that helps someone else open their first envelope today.

Leave a Reply