The reality of living paycheck to paycheck on a $30k salary is tough. Read my personal story and actionable tips to break the cycle and find financial breathing room.

I remember the stress vividly, and it is the reason I am sharing exactly what it felt like living paycheck to paycheck on a $30k salary. That first year out of college, I thought I had made it. I had a degree, a full-time job, and my own apartment. But the reality hit hard by the 20th of every month. My bank account would hover near zero, and I would pray that my car wouldn’t break down or that I wouldn’t get sick.

If you are in that same boat, constantly anxious about money and wondering how to make it to the next payday, I want you to know you aren’t alone. More importantly, I want you to know there is a way out. It isn’t easy, but it is possible. Here is exactly how I navigated the struggle of living paycheck to paycheck on a $30k salary and eventually started building a safety net.

What Does Living Paycheck to Paycheck Actually Mean?

Before we dive into the solutions, let’s define the problem. For me, living paycheck to paycheck on a $30k salary meant that every dollar I earned was already spoken for before I even got it. I would get paid on Friday, and by Monday, the money was gone—rent took half, then utilities, then groceries, and maybe a tiny bit for gas.

There was no buffer. A $60 overdraft fee was a crisis. A flat tire meant putting it on a credit card, which started a new cycle of debt. According to a recent study, a significant number of Americans live this way regardless of income level, but the margin for error is razor-thin when you are earning $30,000. The key is to stop viewing this as a permanent state and start seeing it as a puzzle you can solve .

Step 1: The Brutally Honest Budget Review: Living Paycheck to Paycheck on a $30k Salary

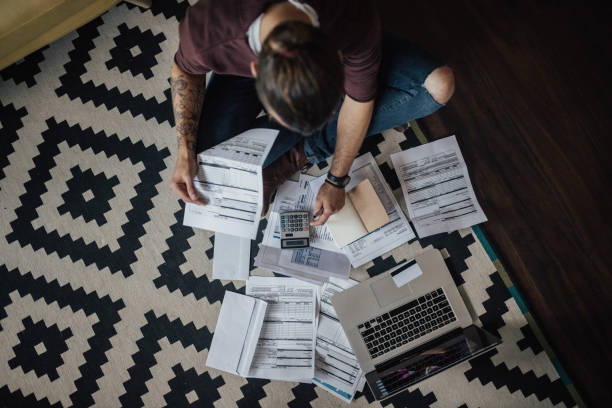

The first step in changing my situation was admitting that I didn’t actually know where my money was going. When you are living paycheck to paycheck on a $30k salary, you often avoid looking at the details because it feels hopeless. I sat down with three months of bank statements and categorized every single expense.

I was shocked. I was spending $150 a month on streaming services I barely watched and energy drinks from the gas station. I wasn’t living large; I was just leaking cash. I used a simple spreadsheet, but you can use a free app like Mint or EveryDollar to track your spending . The goal wasn’t to shame myself, but to find the leaks. Once I saw the numbers in black and white, I could make a plan.

Step 2: Cutting Housing Costs (The Biggest Win)

Housing is, for most people, the largest expense. When you are living paycheck to paycheck on a $30k salary, your rent or mortgage payment is likely eating up a huge chunk of your income—often more than the recommended 30%.

I realized I had two choices: earn more or pay less for housing. I chose the latter first. I found a roommate. It wasn’t my ideal situation at 24 years old, but splitting a two-bedroom apartment cut my housing costs in half. Suddenly, I had an extra $400 a month. If getting a roommate isn’t possible, look into renting a basement apartment or moving to a slightly less expensive neighborhood. Even saving $100 a month makes a difference when you are living on the edge .

Step 3: Mastering the Art of the No-Spend Weekend: Living Paycheck to Paycheck on a $30k Salary

One of the biggest challenges of living paycheck to paycheck on a $30k salary is the social pressure to spend money. My friends wanted to go out for brunch, see movies, or grab drinks after work. Saying “no” felt embarrassing.

I decided to get creative. Instead of going out for expensive coffee, I invited friends over for a potluck dinner. Instead of going to the movies, we had a movie night at home with popcorn I made on the stove. I initiated “no-spend weekends” where I simply didn’t use my debit card from Friday night to Monday morning. I went for hikes, read books from the library, and meal-prepped for the week. This didn’t make me a hermit; it made me intentional. And it saved me over $200 a month .

Step 4: Dealing with Debt While Broke: Living Paycheck to Paycheck on a $30k Salary

It feels impossible to save money when you are living paycheck to paycheck on a $30k salary, especially if you have credit card debt or student loans. The minimum payments alone can drain your account.

I tackled this by using the “snowball method.” I listed all my debts from smallest to largest. I made the minimum payments on everything, but I threw every extra dollar I could find at the smallest debt first. When that one was paid off, I felt a huge rush of motivation. I then rolled that payment into the next smallest debt. This method is less about math and more about psychology . Seeing debts disappear one by one kept me motivated when the journey felt long.

Step 5: Increasing Your Income (The Non-Negotiable)

Budgets and cutting costs will only get you so far. The brutal truth about living paycheck to paycheck on a $30k salary is that $30,000 is a tough number to build wealth on. To truly escape the cycle, I had to increase my income.

I didn’t have a special skill or a business idea. I simply looked for “low-hanging fruit.” I started walking dogs on the Rover app on weekends. I babysat for neighbors. I even signed up for focus groups that paid $50 for an hour of my opinion. This wasn’t a glamorous side hustle; it was just extra work. But earning an extra $150 to $200 a week meant that money could go directly into a savings account. It created the buffer I desperately needed .

Step 6: Building a Tiny Emergency Fund

Experts say you need three to six months of expenses saved. When you are living paycheck to paycheck on a $30k salary, that goal can feel so far away that it’s demotivating. So, I changed the goal. I focused on saving just $500.

I automated a transfer of $20 a week into a separate savings account that I couldn’t easily access. It took me months, but eventually, I hit $500. That $500 was my “break glass in case of emergency” fund. It meant that if my car needed a repair, I didn’t have to use a credit card. It broke the cycle of debt that kept me trapped. Once I had that small cushion, I felt a confidence I hadn’t felt in years .

Step 7: Finding Free Joy

Finally, I had to change my mindset. I was constantly miserable because I felt like I was missing out on life. I learned to separate “cost” from “value.” I realized that some of the best things in life are free or very cheap.

I started checking out books and movies from the public library. I utilized local parks and community events. I learned to cook, which became a hobby that saved me money instead of costing it. Finding joy outside of consumerism is essential when you are living paycheck to paycheck on a $30k salary. It reminds you that your worth is not tied to your spending .

Interactive: Let’s Plan Your First Step

Okay, let’s make this interactive. Thinking about your own situation regarding living paycheck to paycheck on a $30k salary, answer these questions in the comments or on a piece of paper right now:

- The Leak: What is one “small” expense you buy regularly (coffee, snacks, apps) that you could cut or reduce starting tomorrow?

- The Skill: What is one thing you are good at? (e.g., organizing, writing, walking dogs, crafting). Could you monetize this on a platform like Fiverr or TaskRabbit for just 5 hours a week?

- The Goal: What is your “why”? What would having an extra $200 a month allow you to do? Pay off a debt? Go on a small trip? Just feel less stressed?

Conclusion

Escaping the trap of living paycheck to paycheck on a $30k salary is a journey of small, consistent steps. It requires being honest about your spending, getting creative with your free time, and finding ways to increase your income, even a little bit. It took me about two years to go from constantly stressed to having a comfortable buffer. You can do it too.

For more tools, community support, and resources to help you manage your money and build a better financial future, please visit us at evdrivetoday.com. We have guides and a community ready to support you.

Now, I want to hear from you: What is the ONE area you struggle with the most? Is it the budgeting, the loneliness of missing out, or finding the energy to side hustle? Drop a comment below and let’s talk about it. Your story might be the exact encouragement someone else needs to read today.