Meta Description: Learn how to read your first pay stub with this active line-by-line guide. Understand gross pay, deductions, and net pay so you know where your money goes.

Introduction

When you receive your first paycheck, learning how to read your first pay stub becomes essential for understanding your finances. That piece of paper or digital document contains a wealth of information about your earnings and where your money actually goes. Many new employees look at their pay stub and feel confused by all the numbers and abbreviations.

Do not worry—this guide walks you through how to read your first pay stub line by line, explaining every section in plain language. By the end, you will understand exactly why your take-home pay differs from your hourly rate or salary. Mastering how to read your first pay stub empowers you to catch errors and budget accurately. Let us break down this important document together.

What Exactly Is a Pay Stub?: What Exactly Is a Pay Stub?

Before diving into the lines, you must understand what a pay stub actually is. A pay stub is a physical or digital document that accompanies your paycheck and summarizes your earnings for a specific pay period . It details your gross earnings, all taxes and deductions withheld, and the final net pay deposited into your bank account . Today, most employees receive digital pay stubs through an employee portal rather than paper copies . Learning how to read your first pay stub means familiarizing yourself with these five main sections: personal information, pay period, gross earnings, taxes and deductions, and net income . Each section plays a specific role in documenting your compensation.

Section 1: Personal Information

The top portion of your pay stub contains identifying details for both you and your employer. When learning how to read your first pay stub, always start here to verify accuracy.

Your Personal Details

This section includes your legal name, home address, and often the last few digits of your Social Security number or employee ID . Your filing status and number of exemptions from your W-4 form may also appear here . Check that your name is spelled correctly and your address is current. Errors in personal information can lead to tax document problems later.

Employer Information

Your employer’s name and address appear at the top as well . This confirms which company issued the payment. If you work multiple jobs, verifying the employer helps you track which paycheck belongs to which job.

Why This Section Matters

Your filing status determines how much tax your employer withholds from each paycheck . If your status is wrong—for example, listed as single when you are married—you might have too much or too little tax withheld. This directly affects your net pay and potential tax bill in April. Verifying this information is a key part of how to read your first pay stub.

Section 2: Pay Period and Pay Date

The next section clarifies the timeframe your payment covers. Understanding how to read your first pay stub means knowing exactly when you earned the money.

Pay Period Dates

The pay period shows the start and end dates of the work cycle for which you are being paid . For example, it might say “January 1, 2026 to January 15, 2026.” This confirms you are receiving payment for the correct weeks. If you started mid-cycle, verify that the dates match your actual start date.

Pay Date

The pay date is when the payment was issued . This matters for budgeting and tracking when money hits your bank account. Some employers pay on the last day of the pay period, while others pay a week later. Knowing your pay date helps you plan bill payments.

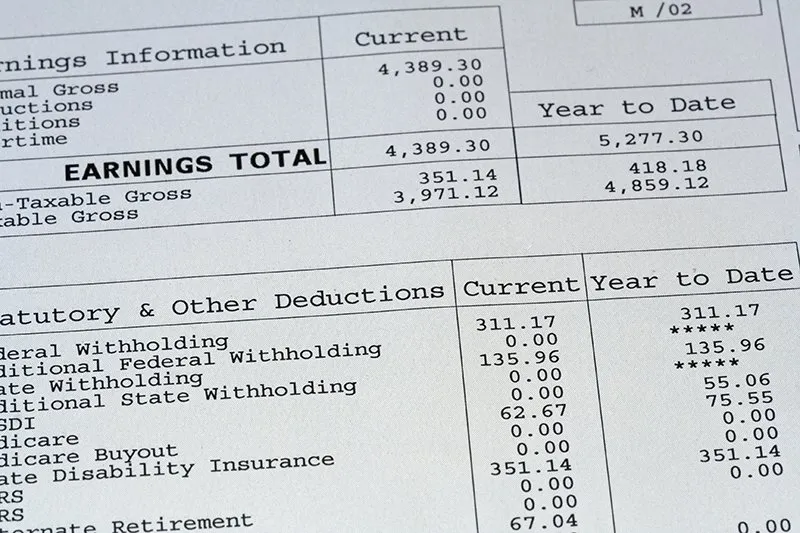

Section 3: Gross Earnings

Now we reach the numbers that excite everyone—your total earnings before anything is taken out. How to read your first pay stub requires understanding that gross pay is not what you actually keep.

What Gross Pay Includes

Gross pay represents the total amount you earned during the pay period . For hourly employees, this section shows your hourly rate multiplied by regular hours worked . Overtime pay appears separately, usually calculated at 1.5 times your regular rate . Salaried employees see a fixed portion of their annual salary for the pay period .

Additional Earnings

If you received any bonuses, commissions, or reimbursements during the pay period, they appear here as separate line items . Some pay stubs also show tips, shift differentials, or various allowances . All these add up to your total gross pay.

Current vs. Year-to-Date

Most pay stubs display gross earnings for the current pay period and the year-to-date (YTD) total . YTD figures accumulate from January 1 through the current pay period . Tracking YTD helps you monitor your annual income progress.

Section 4: Taxes and Deductions

This is where how to read your first pay stub gets really important. Taxes and deductions explain the gap between gross pay and net pay. These fall into two main categories: mandatory and voluntary .

Mandatory Federal Taxes

Federal income tax is withheld based on your W-4 form information . The amount depends on your earnings, filing status, and number of allowances . If too much is withheld, you get a refund in April. If too little is withheld, you may owe money when filing taxes .

FICA Taxes (Social Security and Medicare)

You will see FICA (Federal Insurance Contributions Act) taxes listed separately or combined . Social Security tax is 6.2% of your gross earnings, up to an annual wage base limit . For 2024, that limit is $168,600 . Medicare tax is 1.45% of all your earnings, with no wage limit . High earners may see an additional 0.9% Medicare tax on wages exceeding $200,000 . Your employer matches these contributions, but you only see your portion deducted .

State and Local Taxes

Most states require state income tax withholding, which appears as another line item . Some states have no income tax, while others have flat or progressive rates . Certain cities and counties also impose local income taxes . The amount varies based on where you live and work.

Pre-Tax Voluntary Deductions

Pre-tax deductions are subtracted from your gross pay before income taxes are calculated, reducing your taxable income . Common pre-tax deductions include:

- Health insurance premiums: Your share of medical, dental, or vision coverage

- 401(k) retirement contributions: Money you save for retirement, often with employer matching

- Health Savings Account (HSA) or Flexible Spending Account (FSA): Pre-tax funds for medical expenses

- Dependent Care FSA: Pre-tax dollars for childcare expenses

These deductions lower your tax bill now while providing valuable benefits.

Post-Tax Voluntary Deductions

Post-tax deductions are withheld after taxes are calculated and do not reduce your taxable income . Examples include:

- Roth 401(k) contributions: Retirement savings with after-tax dollars, offering tax-free withdrawals later

- Life insurance premiums: Additional coverage beyond employer-provided basics

- Union dues: Fees for union membership

- Charitable donations: Contributions to nonprofits through payroll

Court-Ordered Deductions

In some cases, you may see deductions for wage garnishments, child support, or alimony . These are mandated by court order and withheld from your pay automatically .

Understanding Deduction Codes

Pay stubs use abbreviations that can confuse anyone learning how to read your first pay stub. Here are common codes :

| Code | Meaning |

|---|---|

| FED, FIT, FWT | Federal income tax withholding |

| STATE, SIT, SWT | State income tax withholding |

| FICA | Federal Insurance Contributions Act |

| SOC, SS, SOCSEC | Social Security tax |

| MED | Medicare tax |

| 401(K) or RET | Retirement contributions |

| INS | Health insurance premium |

| GARN | Garnished wages |

| CHSPPRT | Child support |

Section 5: Net Pay

Finally, we reach the number that actually lands in your bank account. How to read your first pay stub culminates in understanding net pay.

What Net Pay Represents

Net pay, also called take-home pay, is the amount remaining after subtracting all taxes and deductions from your gross pay . This is the money you can spend, save, or invest. Your net pay should exactly match the direct deposit amount or the value of your paper check .

Current and Year-to-Date Net Pay

Like gross pay, net pay typically shows figures for the current pay period and year-to-date . YTD net pay helps you track your actual accumulated earnings for the year.

Why Net Pay Matters for Budgeting

Financial experts agree: base all your spending decisions on your net pay, not your gross salary . If you budget using gross pay, you will overspend because that money is not actually available. Learning how to read your first pay stub teaches you to work with your real take-home amount.

Why You Must Verify Your Pay Stub Regularly

Understanding how to read your first pay stub is not just about curiosity—it protects your wallet.

Catch Errors Early

Payroll mistakes happen. Your hours might be entered incorrectly, your tax code might be wrong, or benefit deductions might not match what you selected . Reviewing every pay stub when you start a new job, and periodically thereafter, helps you catch these errors quickly . If you spot a discrepancy, contact your HR or payroll department immediately .

Verify Tax Withholdings

Major life events like marriage, divorce, or having a child change your tax situation . After updating your W-4, check your pay stub to ensure the new withholding took effect . This prevents surprises at tax time.

Proof of Income for Loans and Rentals

When you apply for a mortgage, car loan, or apartment lease, lenders and landlords often request recent pay stubs as proof of income . They want to verify your earnings are stable and sufficient. Keeping your pay stubs organized makes these applications smoother .

Track Progress Toward Financial Goals

Your pay stub shows year-to-date earnings and deductions, helping you monitor your income and retirement savings progress . If you are aiming to max out your 401(k) contribution, YTD figures tell you how close you are.

Common Questions About Reading Pay Stubs

Why is my net pay so much lower than my gross pay?

The difference comes from mandatory taxes (federal, state, FICA) and any voluntary deductions you chose (health insurance, retirement, etc.) . This is normal and happens to every employee. Learning how to read your first pay stub helps you see exactly where each dollar went.

What if I do not understand a deduction?

Start by asking your HR or payroll department . They can explain what each deduction covers and confirm it is correct. If the issue involves legal matters like garnishments, you may need to consult a wage and hour attorney .

Do independent contractors get pay stubs?

Independent contractors typically do not receive pay stubs from clients because they handle their own taxes and invoicing . However, contractors can generate their own pay stubs using templates to track earnings and provide proof of income for loans .

How long should I keep pay stubs?

Keep your pay stubs until you receive your W-2 at year-end and verify the information matches . After that, retain them for tax purposes or as proof of income. Many experts recommend keeping digital copies for at least three years.

Conclusion

Learning how to read your first pay stub transforms a confusing document into a valuable financial tool. You now understand that your pay stub contains five key sections: personal information, pay period, gross earnings, taxes and deductions, and net pay. Gross pay is your total earnings before anything is removed. Mandatory taxes fund federal, state, and local governments plus Social Security and Medicare. Voluntary deductions pay for benefits you chose, like health insurance and retirement savings. Net pay is the amount you actually take home and should use for budgeting.

Review every pay stub carefully when you start a new job and periodically thereafter. Verify your personal information, check that hours and pay rates are correct, and ensure deductions match your elections. Catching errors early protects your income and prevents headaches later. Your pay stub also serves as proof of income for major life purchases like homes and cars.

Now you have the knowledge to approach your next payday with confidence. No more confusion—just clarity about where your money comes from and where it goes. For more detailed guides on personal finance, career development, and managing your money wisely, visit evdrivetoday.com.

Now it is your turn! What was the most surprising deduction on your first pay stub? Did anything catch you off guard? Share your experience in the comments below. Your story might help another first-time employee understand their own pay stub better.

Leave a Reply