What is FICA? This active guide explains Social Security and Medicare taxes for beginners. Learn how much you pay, why, and what benefits you earn.

Introduction

If you have ever looked at your paycheck and wondered where a chunk of your money went, you are probably asking what is FICA? That abbreviation stands for the Federal Insurance Contributions Act, and it is the law that requires money to be taken out of your pay for Social Security and Medicare . For beginners, understanding what is FICA is the first step to understanding your pay stub and your future benefits.

These taxes fund two massive programs that almost all Americans rely on later in life. Social Security provides retirement, disability, and survivor benefits, while Medicare helps with health insurance costs for people 65 and older . This guide breaks down what is FICA in simple terms so you know exactly where your money goes and what you get in return. Let us dive into the details.

What Is FICA and Why Does It Exist?

To put it simply, what is FICA? It is a federal payroll tax that both employees and employers pay to fund Social Security and Medicare . Congress created this system so that working Americans collectively support the elderly, disabled, and survivors of deceased workers . When you see FICA on your pay stub, it represents your contribution to this social safety net. The government does not keep your money in a personal account for you. Instead, today’s workers pay for today’s beneficiaries, a system called “pay-as-you-go” . Understanding what is FICA helps you see that you are not just losing money—you are investing in a system that will support you or your family when you need it most.

The Two Parts of FICA: Social Security and Medicare

When people ask what is FICA, the answer always has two parts. FICA combines Social Security taxes and Medicare taxes into one deduction on your paycheck .

Social Security (OASDI)

Social Security is technically called Old-Age, Survivors, and Disability Insurance (OASDI) . This part of FICA provides monthly payments to:

- Retired workers who have paid into the system

- Families of workers who have passed away

- People who cannot work due to disabilities

Your Social Security number tracks your lifetime contributions so the government knows what benefits you have earned . The Social Security portion of FICA makes up the larger chunk of what you pay.

Medicare (HI)

The second part of what is FICA involves Medicare, specifically Medicare Part A, which covers hospital insurance . This helps pay for:

- Inpatient hospital stays

- Skilled nursing facility care

- Hospice care

- Some home health services

Medicare taxes fund health coverage for Americans 65 and older, plus younger people with certain disabilities . Unlike Social Security, there is no cap on wages subject to Medicare tax .

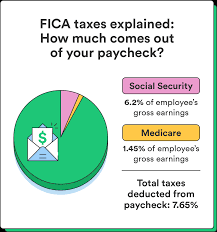

FICA Tax Rates for Employees

So, what is FICA going to cost you from every paycheck? For employees, the total FICA tax rate is 7.65% of your gross wages . This breaks down into two specific rates:

Social Security Portion (6.2%)

Your employer withholds 6.2% of your gross pay for Social Security taxes, up to an annual wage base limit . For 2026, that limit is $184,500 . This means you only pay Social Security tax on the first $184,500 you earn in 2026. Any money you earn above that amount is not subject to the Social Security portion of FICA for the rest of the year .

Medicare Portion (1.45%)

The Medicare tax rate is 1.45% of all your gross wages, with no income limit . Every dollar you earn gets this 1.45% taken out for Medicare.

Example Calculation

If you earn $2,000 in a biweekly pay period, here is what is FICA taking from your check:

- Social Security: $2,000 × 6.2% = $124

- Medicare: $2,000 × 1.45% = $29

- Total FICA withheld: $153

Your employer matches every dollar you pay, contributing another $153 on your behalf . That matching contribution is part of your total compensation package, even though you never see it in your paycheck.

FICA for High Earners: Additional Medicare Tax

For beginners learning what is FICA, the Additional Medicare Tax can be confusing. High earners pay an extra 0.9% on top of the regular 1.45% Medicare tax . This additional tax applies once your earnings exceed certain thresholds:

- Single filers: $200,000

- Married filing jointly: $250,000

- Married filing separately: $125,000

Unlike regular Medicare tax, employers do not match this additional 0.9%. It is paid entirely by the employee . If you earn enough to trigger this tax, your total Medicare withholding becomes 2.35% on earnings above the threshold . Understanding what is FICA at higher income levels helps you plan for accurate withholding.

FICA for Self-Employed Individuals

If you work for yourself, understanding what is FICA changes slightly. Self-employed people pay Self-Employment Contributions Act (SECA) tax instead of FICA . The total rate is 15.3% of your net earnings, which combines:

- 12.4% for Social Security (up to the wage base limit)

- 2.9% for Medicare (all earnings)

Because you are both employee and employer, you pay both halves of the tax. However, you can deduct the employer-equivalent portion (half of the total) when calculating your adjusted gross income on your tax return . This deduction reduces your income tax burden but does not reduce your self-employment tax itself .

For 2026, if you are self-employed, you will pay:

- 12.4% Social Security tax on the first $184,500 of self-employment income

- 2.9% Medicare tax on all income up to the Additional Medicare Tax threshold

- 3.8% Medicare tax (2.9% + 0.9%) on income above the threshold

What You Get in Return for Paying FICA

Understanding what is FICA means also understanding what benefits you earn. This is not just money disappearing—it is buying you future security.

Social Security Benefits

Your FICA contributions qualify you for:

- Retirement benefits: Monthly income starting as early as age 62, with larger payments if you delay up to age 70

- Disability benefits: Income if you become unable to work due to a qualifying disability

- Survivor benefits: Payments to your family members if you pass away

The Social Security Administration calculates your benefit based on your highest 35 years of earnings, indexed for inflation . Higher lifetime earnings generally mean higher monthly benefits, up to a maximum amount.

Medicare Benefits

Paying Medicare taxes through FICA earns you Medicare Part A coverage with no monthly premium when you turn 65, provided you or your spouse worked at least 10 years . Part A covers:

- Inpatient hospital care

- Skilled nursing facility care (limited duration)

- Hospice care

- Some home health services

Most people do pay a monthly premium for Medicare Part B (doctor visits and outpatient care), which is separate from FICA taxes . The Part B premium for 2026 is $202.90 per month .

FICA Wage Base Limits

One key part of what is FICA involves the Social Security wage base. This limit changes nearly every year based on national wage trends .

2026 Social Security Wage Base

For 2026, the Social Security wage base increased to $184,500, up from $176,100 in 2025 . This means:

- You pay 6.2% Social Security tax on the first $184,500 you earn in 2026

- Once your year-to-date earnings hit $184,500, Social Security withholding stops for the rest of the year

No Limit for Medicare

Unlike Social Security, the Medicare portion of FICA has no wage base limit . You pay 1.45% on every dollar you earn throughout the year, no matter how much that totals.

If You Have Multiple Jobs

If you work multiple jobs, each employer withholds Social Security tax as if that job were your only income . This can result in over-withholding if your combined earnings exceed the wage base. When you file your tax return, you get credit for any excess Social Security taxes withheld . This is an important detail when understanding what is FICA in complex employment situations.

FICA Exemptions: Who Doesn’t Pay?

Not everyone pays FICA taxes. Certain groups qualify for exemptions, which is important to know when learning what is FICA .

Common Exemptions Include:

- Students: Students enrolled at least half-time and employed by their school may be exempt from FICA on that income . At West Virginia University, for example, undergraduate students taking 6+ credit hours in fall/spring are FICA-exempt, while graduate students need 5+ credit hours .

- Nonresident Aliens: Foreign nationals in F-1 or J-1 status with nonresident alien tax status are exempt from FICA on wages from employment related to their visa purpose .

- Religious Groups: Members of certain religious sects opposed to insurance may qualify for exemption .

- Some State/Local Government Employees: Certain public employees covered by alternative retirement systems may not pay Social Security taxes.

If you qualify for an exemption, your employer must apply it automatically . You do not need to take action, though you should verify your pay stub shows no FICA withholding if you believe you qualify.

How to Verify Your FICA Withholding

Now that you understand what is FICA, you should check your pay stub to ensure correct withholding.

What to Look For

On your pay stub, look for line items like:

- “FICA,” “SS,” or “Social Security” showing 6.2% withholding

- “MED” or “Medicare” showing 1.45% withholding

- Year-to-date totals to track when you approach the Social Security wage base

Catch Errors Early

Payroll mistakes happen. Your employer might use the wrong tax code, miscalculate your wages, or fail to stop Social Security withholding after you hit the wage base. Reviewing every pay stub when you start a new job and periodically thereafter helps you catch errors quickly . If something looks wrong, contact your HR or payroll department immediately.

Track Your Future Benefits

You can create a my Social Security account online to see your lifetime earnings record and estimated future benefits . This shows you exactly how your FICA contributions translate into future security. It is a powerful motivator to keep paying into the system.

Common Questions About FICA

Is FICA the same as federal income tax?

No. FICA is separate from federal income tax withholding . Income tax funds general government operations, while FICA specifically funds Social Security and Medicare. Your pay stub shows them as separate deductions.

Can I opt out of paying FICA?

Generally, no. FICA is mandatory for almost all workers . The only exceptions are specific exemption categories listed earlier. You cannot choose to stop paying even if you do not plan to collect benefits later.

What if my employer does not withhold FICA?

Employers are legally required to withhold FICA taxes . If your employer does not, they are breaking the law, and you may owe the taxes yourself when you file your return. Report this to the IRS.

Do I pay FICA on tips?

Yes. Tips are considered wages and are subject to FICA withholding . If you receive $20 or more in tips per month, you must report them to your employer so taxes can be withheld.

Why is my FICA different from my coworker’s?

FICA percentages are the same for everyone, but actual dollar amounts depend on your wages . If you earn more, you pay more in FICA taxes, up to the Social Security wage base. Once you hit that limit, your FICA withholding drops because Social Security stops, while your coworker still paying below the limit continues paying the full 6.2%.

Conclusion

Understanding what is FICA transforms a confusing deduction on your paycheck into a meaningful investment in your future. FICA stands for the Federal Insurance Contributions Act, and it funds Social Security and Medicare through payroll taxes . Employees pay 6.2% for Social Security (up to the annual wage base) and 1.45% for Medicare (on all wages), totaling 7.65% . Employers match this amount, and self-employed individuals pay the full 15.3% themselves but can deduct half . High earners pay an additional 0.9% Medicare tax on wages above certain thresholds .

For 2026, the Social Security wage base increased to $184,500, meaning you only pay Social Security tax on the first $184,500 you earn . Medicare taxes apply to every dollar, with no cap . In return for these taxes, you earn retirement, disability, and survivor benefits through Social Security, plus hospital insurance coverage through Medicare when you turn 65 .

Now you can look at your pay stub with confidence. You understand exactly where that money goes and what benefits you are building for the future. For more detailed guides on personal finance, taxes, and making the most of your money, visit evdrivetoday.com.

Now it is your turn! Were you surprised by how much goes to Social Security versus Medicare? Did you know about the Additional Medicare Tax for high earners? Share your thoughts and questions in the comments below. Your questions might help another beginner understand what is FICA better.

Leave a Reply