Ready for a financial upgrade? Learn the exact process for migrating from traditional budgeting to zero-based as a freelancer to gain total control over your variable income.

If your current budget only tracks what you already spent, you are missing the point. You need a system that plans where your money goes before you spend it. That is why migrating from traditional budgeting to zero-based as a freelancer transforms your financial life. Traditional budgets look backward. Zero-based budgeting looks forward. It forces you to assign every dollar a job based on the money you have right now. For freelancers with irregular income, this shift proves essential. This guide walks you through five practical steps to make the switch smoothly and successfully.

Why Traditional Budgeting Fails Freelancers

Traditional budgeting often involves looking at last month’s spending and setting similar limits for this month. This reactive approach does not work when your income fluctuates wildly. Migrating from traditional budgeting to zero-based as a freelancer solves this problem. Zero-based budgeting ignores the past. It focuses on the present. You budget only the cash you currently hold, assigning it to expenses, savings, and goals until you reach zero. This proactive method prevents overspending and builds financial discipline .

The Mindset Shift Required

Changing your budget requires changing your thinking. Traditional budgets feel passive. You record what happens. Zero-based budgeting feels active. You decide what will happen. This mindset shift is the core of migrating from traditional budgeting to zero-based as a freelancer. You stop asking, “Where did my money go?” and start asking, “Where will my money go?” You take the driver’s seat. This proactive stance reduces anxiety and increases intentionality. You become the boss of your money, not its historian.

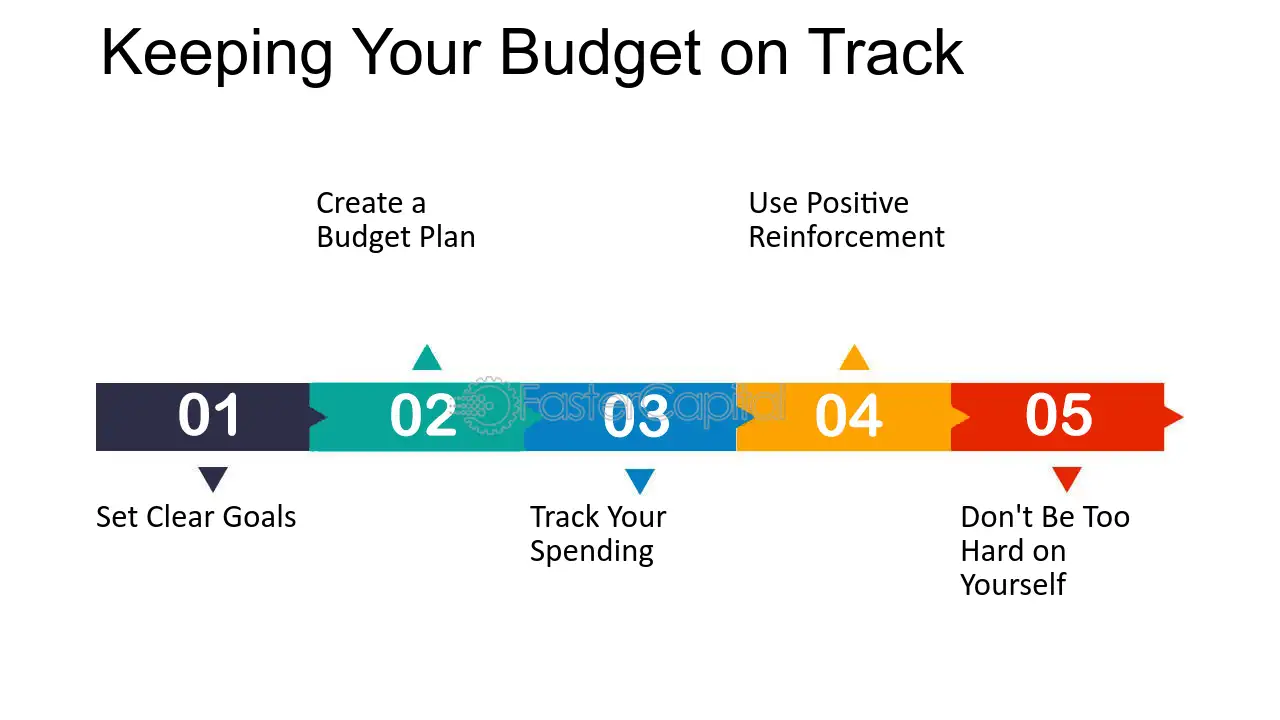

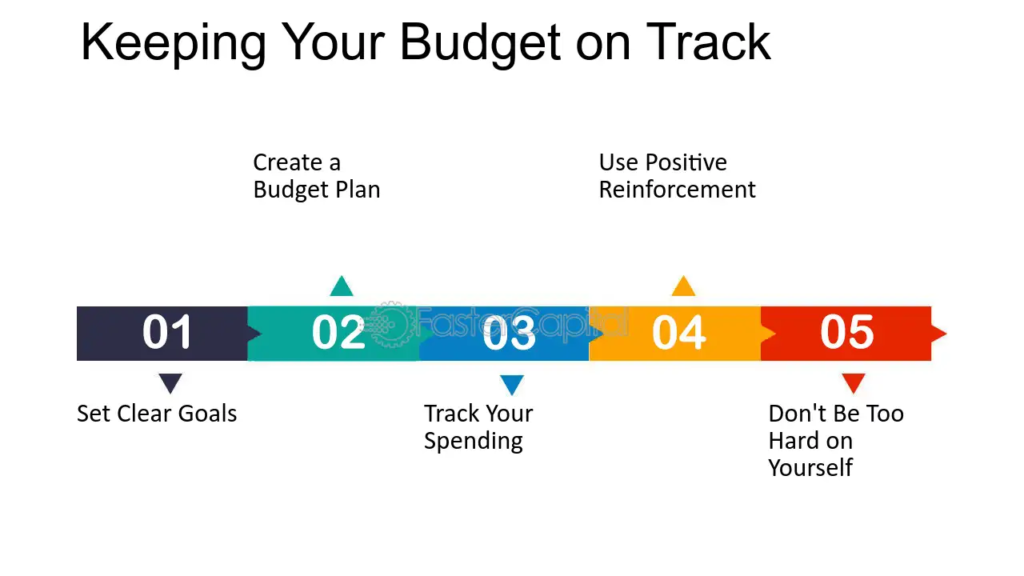

Step 1: Track Your Current Spending for One Month

Before you can switch, you need data. Spend one month tracking every single expense. Use a notebook, an app, or a simple spreadsheet. This step in migrating from traditional budgeting to zero-based as a freelancer provides a baseline. You learn your true spending habits. You see where your money actually goes versus where you think it goes. Categorize everything: rent, groceries, coffee, software subscriptions, client lunches. This information guides your first zero-based budget. Without it, you guess. With it, you plan intelligently.

Step 2: List All Your Income Sources and Expenses

Now, list everything. Write down every possible income source: client payments, retainers, affiliate income, side hustles. Then, list every expense category. Divide them into fixed (rent, insurance) and variable (groceries, dining out). Include business expenses and tax savings. This comprehensive list forms the foundation for migrating from traditional budgeting to zero-based as a freelancer. Do not leave anything out. The more complete your list, the more accurate your budget.

Step 3: Prioritize Your Expenses

Zero-based budgeting requires prioritizing. Not all expenses hold equal weight. In this phase of migrating from traditional budgeting to zero-based as a freelancer, you rank your needs. Essentials come first: housing, utilities, food, transportation, minimum debt payments. Next come business expenses and tax savings. Then savings goals and debt repayment above minimums. Finally, discretionary spending like entertainment and dining out. This hierarchy ensures your most important obligations receive funding before anything else.

Step 4: Assign Every Dollar a Job

Here is where the magic happens. Take your current income—the money in your bank account right now. Start assigning it to the categories you listed, in order of priority. Assign until you reach zero. Every dollar has a purpose. This is the essence of migrating from traditional budgeting to zero-based as a freelancer. If you run out of money before covering all categories, you must cut back on lower priorities. If you have money left after covering everything, assign the surplus to savings, debt, or a buffer fund.

Step 5: Review and Adjust Weekly

Your first zero-based budget will not be perfect. That is okay. The key to successful migrating from traditional budgeting to zero-based as a freelancer is regular review. Schedule a weekly money date. Compare your actual spending against your budget. Did you overspend on groceries? Adjust next week’s dining out budget to compensate. Did a client payment arrive unexpectedly? Assign those new dollars immediately. This weekly check-in keeps your budget accurate and relevant. It turns budgeting into a habit, not a chore.

Handling Variable Income During the Transition

Variable income poses the biggest challenge during migrating from traditional budgeting to zero-based as a freelancer. You cannot budget money you do not have. The solution? Budget only what is in your account today. If you have a slow month, your budget covers only essentials. In high-income months, you allocate surplus to savings, taxes, and building a buffer. This buffer then protects you during future slow months. This approach, often called “income smoothing,” stabilizes your finances .

Building Your Buffer Fund

A buffer fund proves essential when migrating from traditional budgeting to zero-based as a freelancer. This is a separate savings account that holds extra cash. In months you earn more than your baseline expenses, the surplus goes here. In months you earn less, you draw from this buffer to cover your budget. Aim to build a buffer equal to one to three months of essential expenses. This cushion transforms your variable income into a steady, predictable cash flow .

Common Challenges and How to Overcome Them

Migrating from traditional budgeting to zero-based as a freelancer comes with hurdles. One common challenge is underestimating variable expenses. Your first few months may require adjustments. Build flexibility into your budget. Another challenge is forgetting irregular expenses like annual software subscriptions. Solve this by dividing annual costs by 12 and saving that amount monthly in a sinking fund . Finally, do not get discouraged by early mistakes. Every budget teaches you something. Keep refining.

Tools to Simplify Your Migration

You do not have to do this alone. Many tools assist with migrating from traditional budgeting to zero-based as a freelancer. YNAB (You Need A Budget) is specifically designed for zero-based budgeting and handles variable income beautifully . EveryDollar offers a simple interface for assigning every dollar . Goodbudget digitizes the envelope system . Use these tools to automate tracking and simplify the transition. Find one that fits your style and stick with it.

The Role of Sinking Funds

Sinking funds are your best friend during migrating from traditional budgeting to zero-based as a freelancer. These are savings categories for specific future expenses. Examples include holiday gifts, quarterly taxes, new equipment, and vacation. You contribute a small amount each month. When the expense arrives, you have the cash ready. This prevents large, irregular bills from blowing up your budget. Sinking funds embody the proactive spirit of zero-based budgeting.

Tax Planning in Your New Budget

Taxes often trip up freelancers during migrating from traditional budgeting to zero-based as a freelancer. You must include tax savings as a non-negotiable category. Calculate your estimated tax rate (typically 25-30% of profit). Each time you receive income, immediately transfer that percentage to a separate tax savings account. Treat it like any other bill. When quarterly estimated taxes come due, you pay them without stress. This habit prevents April surprises and keeps you compliant.

Celebrating Small Wins

Migrating from traditional budgeting to zero-based as a freelancer represents significant personal growth. Celebrate your progress. Did you successfully budget a whole month? Celebrate. Did you build your first $500 buffer? Celebrate. Did you pay quarterly taxes on time without scrambling? Celebrate. These small wins build momentum. They reinforce your new habits. They remind you why you made the switch. Acknowledge your effort and keep moving forward.

The Long-Term Benefits of Zero-Based Budgeting

Once you complete migrating from traditional budgeting to zero-based as a freelancer, the benefits compound. You experience less financial stress. You make intentional spending decisions. You build savings consistently. You handle slow months without panic. Your business becomes more profitable because you track expenses closely. Your tax time becomes simple because you saved all year. This system transforms your relationship with money. It empowers you to build the freelance life you want.

Conclusion

Making the switch transforms your financial future. By migrating from traditional budgeting to zero-based as a freelancer, you take control. You stop reacting to the past and start directing your future. Follow these five steps: track spending, list everything, prioritize, assign every dollar, and review weekly. Build your buffer. Use helpful tools. Plan for taxes. Celebrate your wins. This new system brings peace and stability to your freelance finances. Start today. For more resources, tools, and community support tailored to freelancers like you, visit evdrivetoday.com.

Share Your Transition Story! Have you made the switch to zero-based budgeting? What challenges did you face? What tips would you share with someone just starting? Drop a comment below and let us learn from your journey. Your experience could inspire another freelancer to take control of their money.

Leave a Reply